6 September 2023

Author: Gavyn Davies, Executive Chairman

Main Points

- Global asset markets in August were impacted mainly by a rise in real bond yields in the US, led by a change in perceptions about the strength of activity growth in the American economy.

- US 10-year bond yields have risen by almost 50 basis points from mid-July to the end of August, most of which stemmed from a rise in real yields, with very little change in breakeven inflation. There has been a moderate bear steepening (i.e., dis-inversion) in the yield curve in the US, with little change in yields in the EU and elsewhere.

- Fulcrum’s models interpret these events as a tightening in “unconventional” monetary policy, triggered by a combination of firmer activity in the US and a rise in oil prices, both of which reduce the likely extent of Fed rate cuts next year.

- Because the change in unconventional monetary policy has been larger in the US than in Europe or Asia, the dollar has been firm, with the overall dollar index rising by 2% in the last month.

- These events also constituted a pause in the regime of supply side improvements that have dominated global markets and helped risk assets for lengthy periods since October 2022. Hence there has been a small decline in equity indices, with the Standard and Poor’s 500 (S&P 500 Index1) falling slightly in the past month.

- The final week of August showed some reversal of these shifts in asset prices, suggesting that the markets might be shifting back to the supply-friendly interpretation of the global economy that dominated markets until July.

- Looking forward, the main regimes that will impact markets are not very clear, so caution is The strength of US activity, relative to Europe and China, seems likely to continue for a while, in which case US real yields and the dollar would probably continue to rise somewhat.

- However, this “no landing” regime could shift back towards a soft-landing scenario if the US economy slows in 2023 Q4, especially if supply side gains in the US labour market are maintained. A prolonged rise in oil prices above their recent $90/barrel ceiling is the main risk factor that could tilt the markets towards a harder landing.

Blip in the Balanced Portfolio Last Month

The strong performance by so-called “balanced” portfolios so far in the 2023 calendar year has been somewhat surprising to many macro economists, in view of the combination of recession and inflation risks that seemed prevalent at the start of the year. Calendar year returns have been dominated by global equities, which have risen by 16%2 so far. Among equities, notable gains have come from Japan (27%)3 and the Nasdaq (35%)4, while lower returns have been seen in the EU (16%)5, UK (1%)6 and especially China (-6%)7. Global bonds (hedged to USD) have offered returns of 3%8, while commodities (in USD) have returned -3%9.

Overall, these asset market results have resulted in year-to-date returns of 10% in a balanced portfolio (consisting of 50% global equities, 40% global bonds and 10% commodities). In retrospect, this excellent performance was driven mainly by dis-inflation, fuelled by significant supply side gains. These supply improvements were, in turn, driven by

- Lower commodity prices, notably oil

- Rising labour force participation

- Better matching between unfilled vacancies and unemployed workers in the labour market, leading to a vertical shift downwards in the Beveridge Curve, and

- Repairs to supply chains fractured during the pandemic

In addition to these global factors, there were major regional forces at work, including optimism about AI in the US, disappointing activity data from China and the EU, and extremely easy monetary policy conditions in Japan.

In contrast to these strong positive year-to-date returns, balanced portfolios recorded a minor setback in August, declining by about 4% at one stage.

What were the main drivers during August? Among several candidates, we would highlight the following:

- Oil prices rose strongly during the month, reflecting tighter supply conditions in the global With the Saudis showing little sign of ending their “temporary” cut in supply of 1 mb/d, the market could push the price of Brent oil above the recent $90/barrel ceiling in coming months. This would represent a significant supply side deterioration for the global economy and risk assets.

- Growth in the US economy is showing signs of rising in 2023 Q3, notably in the Atlanta Fed GDPNow projection for the quarter which remains at 5.6%. This may delay the prospect of any easing in monetary policy by the Fed, even if policy rates do not rise again this year.

- The surge in the federal budget deficit in the US has continued apace. It now seems likely that the deficit in FY 2023 will reach almost 8% of GDP, almost double last year’s This could explain some or all of the rise in US real bond yields this year. (See this article.)

- In sharp contrast to recent activity data in the US, China has slowed further in August, and the imploding real estate sector clearly needs more policy support from the government. This support does seem to be on the agenda but is being delivered very cautiously at present. We assume that further stimulus will result in GDP growth close to the 5% target in 2023.

- Activity in the EU has deteriorated further, especially in Germany, where the collapse in manufacturing is now spreading to the services sector. Germany may well fall into recession before year end, but the EU as a whole may narrowly avoid that fate.

While these factors have undoubtedly contributed to the decline in risk assets in August, a major market setback has so far been avoided. There has been one major economic factor pulling in a more optimistic direction. This is the continuing downward path for core inflation in the US, along with further large improvements in labour force growth (due to rising immigration and labour participation) and in labour productivity. It is possible that these supply side improvements will be powerful enough to offset the adverse factors listed above, leading to a soft landing for the US and global economy. This, in fact, is exactly what has been happening for much of the current calendar year.

The Three Possible “Landings”

One productive method of analysing how the current economic cycle might proceed is to consider whether the next stages will be characterised by a soft landing, a hard landing, or a “no landing” scenario. The different regions of the world may well behave differently in this regard but (as usual) the US is likely to prove dominant for global markets.

In order to make the discussion relevant to medium-term views about markets, we focus on the possible flow of new economic information at the 3 to 6 months horizon. Any attempt to predict the “final” destination of the cycle is much more hazardous, both in terms of the lengthy time horizon involved and because there are dangers that the global economy might appear for interim periods to be on a path that does not in fact transpire by the end of the cycle. For example, it is arguable that the asset markets have shifted towards pricing a soft landing in 2023, even though the eventual outcome in (say) 2025 might turn out to be very different. For Fulcrum’s main investment horizon, it is the markets’ medium-term direction that matters.

There are three main scenarios in the next 3-6 months:

- A Soft Landing. This would be defined as a situation in which the market shifts its expectations towards a slowdown in the US economy, and a softening in the labour market, without a recession. Core price inflation and wage inflation would remain on a downward path, consistent with a return of Personal Consumption Expenditures (PCE) headline inflation to the Fed’s 2% target over the next two years. Unemployment would rise moderately, consistent with eventually reaching a maximum rate of 4.5% late in the cycle. The Fed would be expected to reduce nominal interest rates broadly in line with the decline in core inflation, possibly with a lag. In response to these economic developments, the inversion in the yield curve would become far less extreme, and the curve may shift towards a more normal upward slope. Returns at the long end of the bond market may become positive, but are unlikely to become extremely attractive, since the normal recessionary end to the cycle would be avoided or delayed. For the same reasons, equity returns would likely be attractive, despite high starting valuations. In a risk-on environment, the dollar would probably weaken though this would depend on activity growth in regions outside the US.

- A Hard Landing: This would be the polar opposite development, in which the markets would shift their expectations towards an imminent recession in the US, with dislocations in consumer and business confidence and declines in risk appetite across the financial system. This would imply that the Fed has engaged in overkill, with the lagged effects of tighter monetary conditions and the credit squeeze finally becoming visible. Real GDP growth would turn sharply negative for at least two quarters, and unemployment would rise rapidly towards a maximum level of 5.5%. Fed policy would ease abruptly, with policy rates dropping by 300-400 basis points within one year. The yield curve would steepen dramatically, with long term yields embarking quickly on a path towards 2-2.5% yields. Credit spreads would widen across the entire credit space, especially in below investment-grade areas. In a risk-off environment, the dollar might strengthen for a while, but equities would fall to new lows for the cycle, possibly bottoming at around 3000 for the S&P 500 index.

- A No Landing Scenario. This would be a scenario in which market expectations shift towards firmer growth and higher core inflation in the US economy, raising awkward questions about whether the Fed has done enough to kill medium term inflation This scenario would be triggered by the continuation of above-trend GDP growth, probably running at above 3% for a further period after the end of 2023 Q3. The softening in the labour market would begin to reverse, with growth in non-farm payrolls rising to 250,000 or more. Unemployment rates would fall towards 3%, and wage inflation would re-accelerate. Core price inflation would become stuck at around 4%, with the Fed having to admit that it would be likely to miss its 2% inflation target for a very prolonged period ahead. In consequence, the Federal Open Market Committee (FOMC) would need to raise policy rates towards 6-6.5%, and that would drag bond yields towards 4.75-5.0%, with rising real yields fueling most of these increases in interest rates.

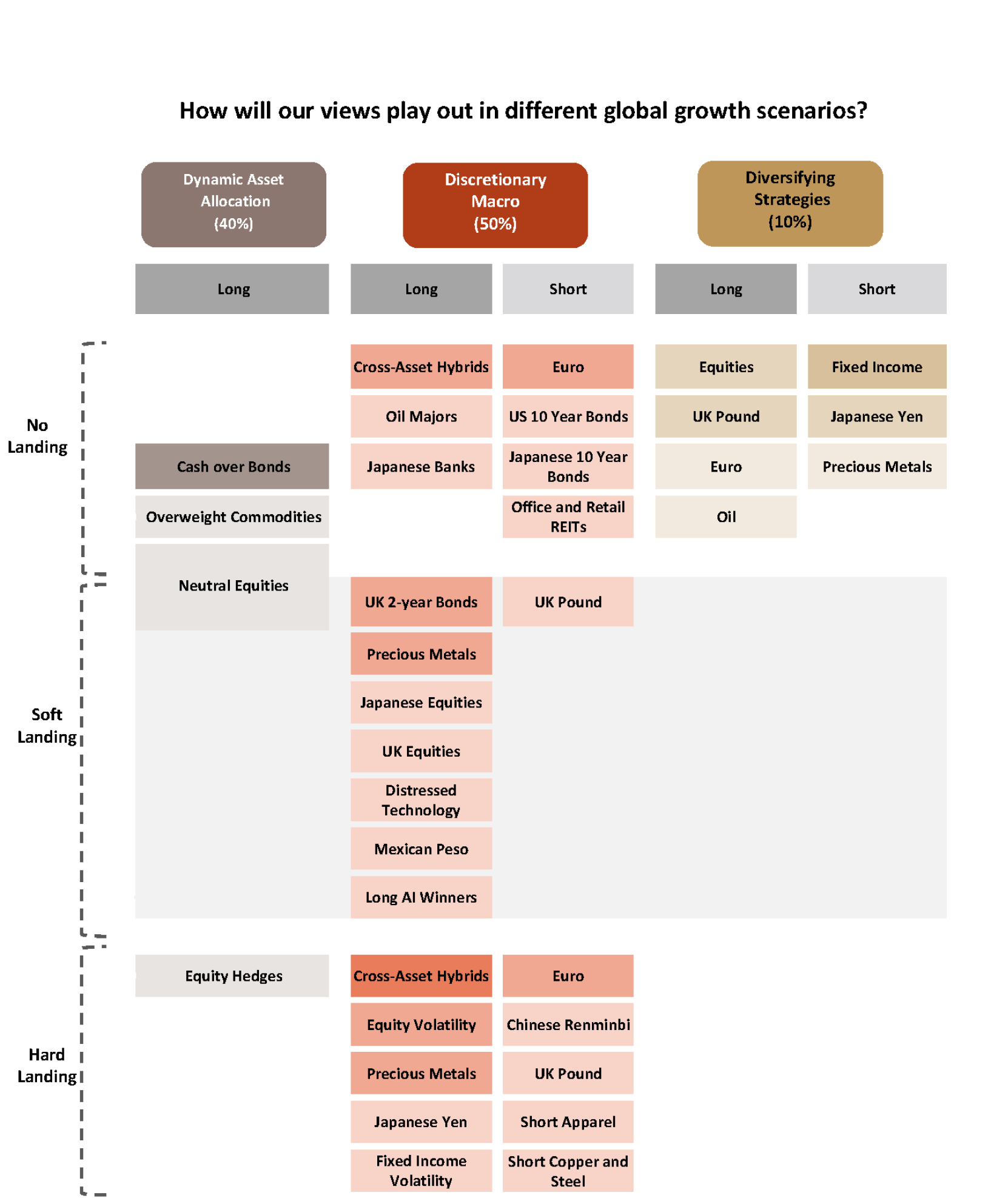

Suhail Shaikh, Fulcrum’s CIO, has produced detailed analysis of how these three scenarios might play out for the three component segments of the Diversified Absolute Return Fund in the appendix below.

Conclusion

The final and most difficult step needed to complete this analysis is to assess probabilities to each of the three possible broad scenarios outlined above. Recall that the intention is to consider the likely flow of economic information in the next 3-6 months, not the eventual destination of the economic cycle at some uncertain date in the more distant future.

Although Fulcrum’s macroeconomic models provide essential inputs into these considerations, discretionary judgement is also required to reach an assessment at present. We currently judge that there is a 60% likelihood that a soft-landing scenario will become dominant in the next 3-6 months, a 30% likelihood of a no landing scenario and a 10% likelihood of a hard landing scenario. It is likely that Fulcrum’s asset market views will continue to be impacted substantially by further developments in this assessment.

Appendix

Source: Fulcrum Asset Management LLP. As at 5th September 2023.