The Fed’s Internal Debate on the Bond Market Debacle

Although the rise of 136 basis points in long dated bond yields in the past 6 months has been remarkable by any standards, the leadership at the Fed did not comment very much upon the matter until the Federal Open Market Committee (FOMC) meeting on 20 September. In retrospect, this was something of an oddity, especially since the entirety of the rise in yields was explained by the increase in real yields, not breakeven inflation rates.

Our models, however, did not ignore the implications of this earthquake in the bond market, and they viewed it as a significant tightening in “unconventional” monetary policy. The models are heavily influenced by changes in the shape of the yield curve, and they were impressed by the fact that longer dated yields were rising faster than shorter dated yields, with the yield curve dis-inverting during a bear phase in the bond market.

This form of unconventional monetary policy normally involves either changes in the size of the Fed’s balance sheet, or guidance about the likely forward path for short rates, or both.

This time, there has been a combination of both factors, with the Fed embarking on a program of quantitative tightening (QE) in June 2022 and some modest guidance about “high-for-longer” policy rates throughout the summer of 2023. QT might have been the main factor in this episode since the current program has proceeded more rapidly than the previous episode of QT in 2018-19. Along with other factors, including the rise in the budget deficit, the resolution of the debt ceiling crisis in July, and the relaxation of yield curve control in Japan, the Fed’s QT changed the balance of supply and demand in the Treasury market and caused yields to rise markedly.

In late September, these market adjustments finally proved too large for the Fed leadership to ignore. Chair Powell’s remarks about the equilibrium real policy rate (r*) at the press conference were new and important.

Furthermore, since Powell lifted the lid on the debate last month, there have been further FOMC speeches on the bond sell-off. While Powell’s remarks remain the benchmark speech on the bond debacle, there have been new interpretations that complicate the picture in recent days.

In summary:

- At the FOMC, Powell said very clearly that r* has probably risen because GDP growth has been sustained at higher levels for longer than the Fed expected. He also hinted that the supply side in the labour market was improving. These remarks, on net, implied a high-for-longer path for short rates in the next year or two. The Summary of Economic Projections marked GDP growth higher than seen in June but failed to be impressed by lower core inflation in recent months and therefore also marked policy rates higher. Even if this form of hawkish forward guidance was partly unintentional, it proved clearly bearish for bonds. Because the impact of higher GDP growth was clearly acknowledged, the press conference seemed to us to be more neutral for equities, though equities hit new lows in early October.

- The September payrolls number on 6 October was the next key turning point. While confirming the high-growth story, the low print on hourly earnings and increases in labour supply obviously supported Powell’s optimistic remarks about the supply side of the labour market. Combined with declining oil prices, equities rallied while bond yields fell below 4.7%.

- Since the payroll report, there have been several FOMC speeches which have started to provide more detailed thinking on how the FOMC might judge Powell’s assertions at his press conference. In particular, there have been two important speeches by Lorie Logan (Dallas Fed President) and Philip Jefferson (Board of Governors), which carry a remarkably similar message. This apparent co-ordination could represent the beginning of a new broader consensus on the committee, though it is far too early to be sure of that. We will learn a lot more from other speakers before the month end.

- Logan/Jefferson (LJ for short) have accepted Powell’s conclusion that r* may have risen because of firmer GDP growth in recent months. However, they have both made a key new point that is important for equities and bonds. For LJ, the FOMC needs to distinguish between two different drivers for higher bond yields.

- If bond yields are being pushed higher by higher GDP growth and high-for-longer short rates, then the FOMC should allow this to take place, since a tighter Financial Conditions Index (FCI) will be needed to keep inflation on track. This is the r* channel that Powell discussed.

- If, however, bond yields are being pushed higher because the term premium is rising – possibly because of supply/demand imbalances in the bond market – then the situation is different, in the minds of LJ. Higher bond yields driven by the term premium can tighten financial conditions without this being driven by an increase in GDP growth. LJ both remark that this tightening in the FCI might occur because corporate bond yields and mortgage rates increase, but they are also focused on the possibility that lower equity prices may be part of the process.

- LJ both suggest explicitly that a rise in bond yields driven by the term premium and declining risk appetite – which is exactly what is happening (see graphs below) – would imply that the bond markets and the FCI are doing some of the Fed’s work for it, in which case they would be much more reluctant to “validate” any rise in bond yields by raising short rates. In fact, they might even think about doing the opposite, though they definitely do not countenance any early reduction in short rates.

Conclusion

These speeches and other Fed remarks represent very early-stage FOMC thinking, and the conclusions discussed above will not go mainstream reflected in Powell’s next press conference on 1 November. However, this direction of Fed commentary does indicate that the FOMC might push in a more dovish direction if bond yields continue to be increased via the term premium, especially if equities drop at the same time. This, along with a flight to safety in bond markets because of the serious nature of the Middle East conflict, seems to have changed the direction of real yields, for now at least.

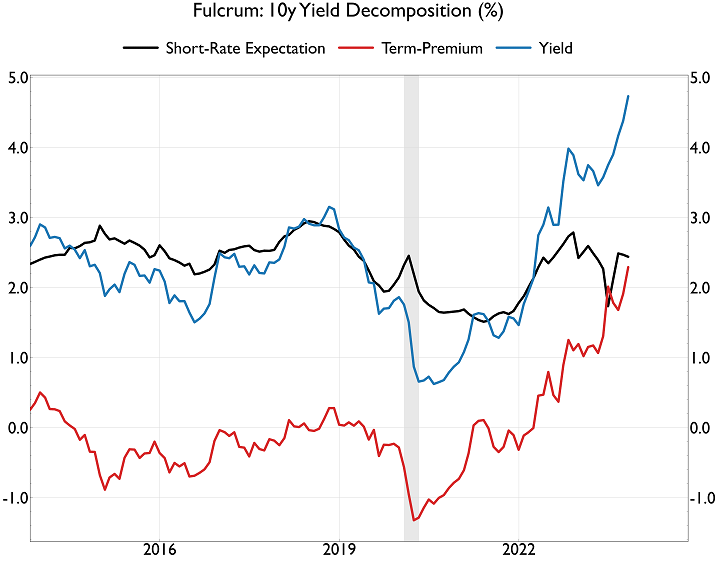

Graph 1

Note: The Fulcrum model uses consensus survey data on short-rate expectations over the next 10 years to back out an estimate of the term premium.

Note: The Fulcrum model uses consensus survey data on short-rate expectations over the next 10 years to back out an estimate of the term premium.

Source: Fulcrum Asset Management

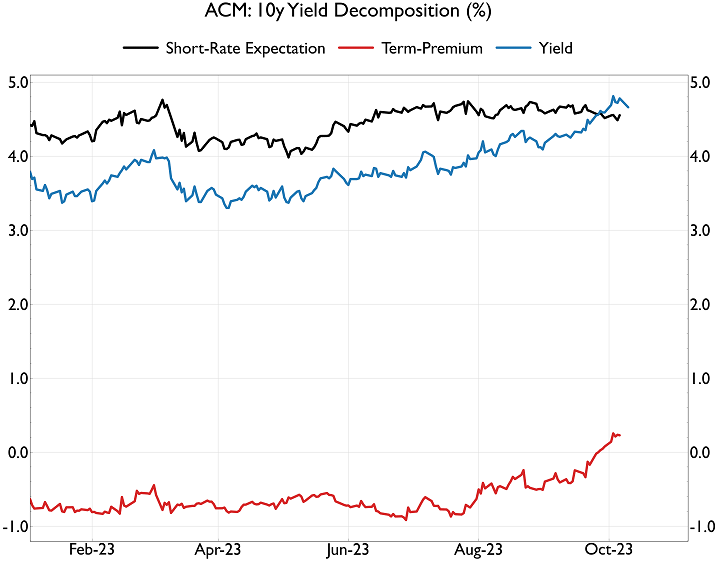

Graph 2

Note: The ACM model estimates a 5-factor no-arbitrage model of the Treasury yield curve using principal components analysis.

Source: Haver Analytics

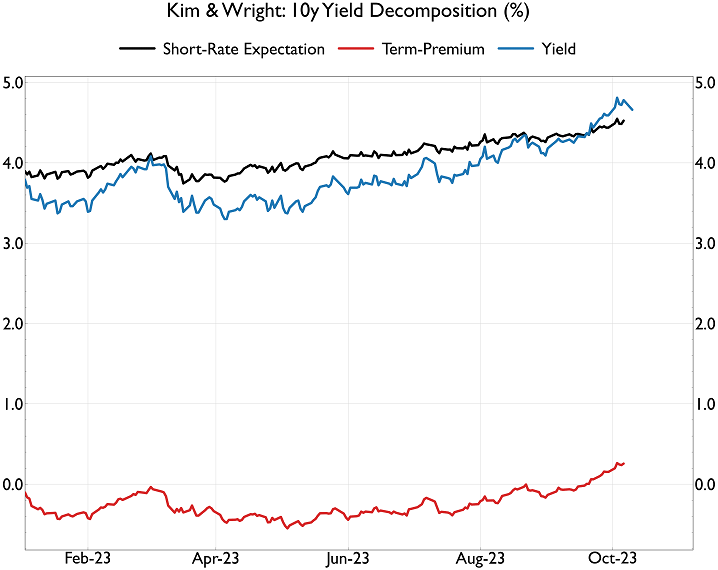

Graph 3

Note: The Kim & Wright approach use a 3-factor no-arbitrage model that is augmented with survey data.

Source: Haver Analytics