Fulcrum Recession Model and the Sahm Rule

The slowdown in US activity in recent weeks is not unexpected but it makes it more difficult to distinguish between two scenarios:

a) A benign shift in the economy, away from “no landing” and towards a soft landing; versus

b) The onset of a recession.

These two very different scenarios are observationally equivalent right now. How can we distinguish between them?

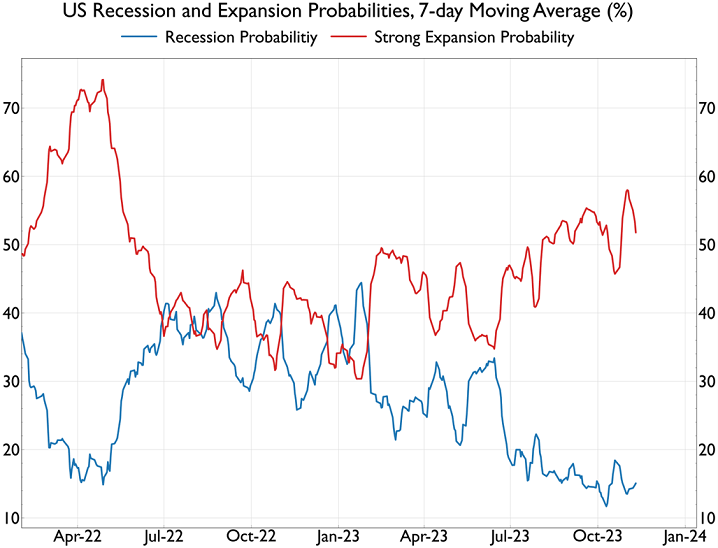

The Fulcrum nowcast model would be our preferred way of approaching this problem since it is specifically designed to estimate the current growth rate and the volatility of economic activity. This enables us to measure recession risk (in the next 12 months) on a real time basis (see Graph 1). The latest probability of a recession is estimated to be 16%, up from a (very) temporary low point of 8% in August. Although slightly higher than the low point, the estimated probability of recession has not broken above the range that has been in place throughout the summer. Having said that, there has been a noticeable fall in the activity growth rate itself in the nowcast. This dropped to 1.6% last week, about a percentage point lower than shown at the end of October.

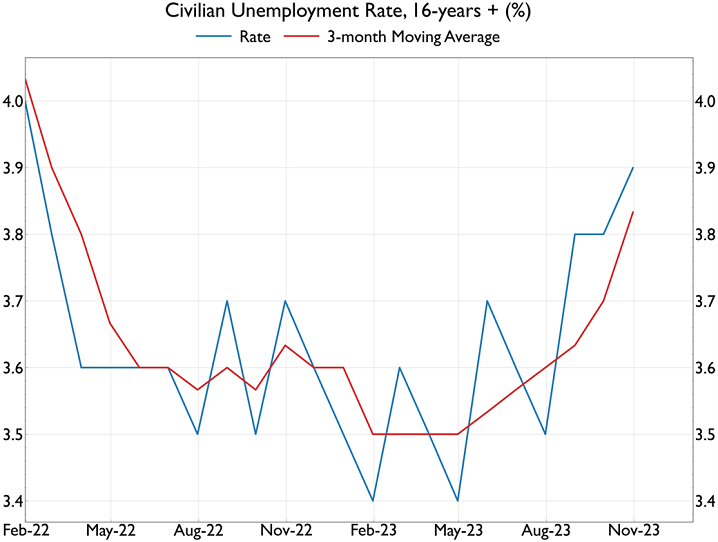

The Sahm Rule is another way of approaching this problem. Based on the work of Claudia Sahm, the rule sets a threshold for the recent rise in unemployment which in the past has signalled an imminent recession.

Her particular version of the rule says that a recession has started when the 3-month moving average for the unemployment rate (3MMA) exceeds by 0.5 percentage points the low point in the 3MMA over the past 12 months. The latest unemployment rate (3.9% in October) produces a 3MMA of 3.8%, which is 0.33 pp (unrounded) above the threshold of 3.5% reached in April. In order to exceed the threshold, the rate would need to rise to 4.3% next month or be sustained above 4% for several months to come (see Graph 2).

How reliable is this rule? A slightly different version was first popularised not by Claudia Sahm but by Bill Dudley in the 1990s, and it has worked well out of sample since then.

However, Claudia Sahm herself has suggested that the recent behaviour of the labour market may prove to be different from previous cycles. This time, the unemployment rate is rising not because of a sharp rise in layoffs but because of an unexpected rise in the labour force, due to immigration and a large rebound in the participation rate of prime age workers, notably females and Black Americans. Ms Sahm says this may result in a temporary rise in unemployment, followed by an early decline as the extra workers are absorbed into jobs. If that is the case, the rule could be breached in the current cycle without signalling a recession.

In her recent blog on Substack, Ms Sahm suggested that she had “created a monster”, adding that the rule is “not a law of nature” and advised “don’t bet on it”. Nevertheless, it is receiving a great deal of attention in the markets at the moment.

If the Sahm Rule is breached in coming months, which is very likely, it should be seen as an amber, not a red, signal. This cycle is different in many ways, and the rule is overly simplified in my view, and offers fake precision. However, if any future rise in unemployment is driven by layoffs instead of labour force growth, the signal would probably be a much darker shade of amber. This aspect of the data needs to be watched carefully in coming months.

Morgan Stanley’s economics team has suggested that a Sahm-type rule should be expressed not by reference to the unemployment rate but by reference to the employment-to-population rate. These concepts both measure slack in the labour market and are usually very closely (and negatively) correlated to each other. However, if the labour market slackens because of a rise in the labour force, the unemployment rate would rise while the employment rate would not fall very much, if at all. Therefore, the latter concept might avoid the danger of a misleading signal on a Sahm-type rule. This is indeed suggested in recent data, and we will be monitoring monthly developments in this series going forward, in parallel with the simple Sahm rule.

In conclusion, recession triggers have not yet been breached either in the Fulcrum nowcast model or in different versions of the Sahm rule. However, both Fulcrum and Sahm models are much closer to critical levels than they were in 2023 Q3, so my own confidence in ruling out an imminent recession, which has been very high, has accordingly dropped a bit.

Graph 1: Fulcrum Recession Model

Source: Fulcrum Asset Management

Graph 2: Trigger for the Sahm Rule

Source: Haver Analytics

Note: The recession rule is triggered when the 3MMA for unemployment (ie the red line) has risen by at least 0.5 PPts compared to its low point in the previous 12 months.